Technical Team, SMSF Association

Now that 1 July 2017 has passed, applying CGT relief is at the forefront of every advisor’s mind. Read in conjunction with and taking parts from the SMSF Association’s ‘Go-To Guide on CGT Relief’ this document should help further clarify the process involved in the application of segregated CGT relief.

How it works? See the SMSF Association’s Go-To Guide for more

CGT relief allows trustees to elect to reset the cost base of assets that will no longer be eligible to support superannuation income streams in retirement phase from 1 July 2017 to their market value. This effectively “locks-in” the tax-exempt CGT treatment of assets that supported a pension up to 30 June 2017 before the transfer balance cap (TBC) applies and the transition to retirement income streams (TRIS) taxation changes took effect.

It will be critical to determine which method an SMSF is eligible to adopt by its make-up during the ‘precommencement period’. The ‘pre-commencement period’ begins on 9 November 2016 to just before 1 July 2017.

Are you eligible for CGT relief?

The object of the CGT relief provisions is to provide temporary relief from certain capital gains that might arise as a result of individuals complying with the transfer balance cap, or TRIS reforms, which commenced on 1 July 2017. The legislation with respect to this relief is contained in Subdivision 294B of the Income Tax (Transitional Provisions) Act 1997 (ITTP 1997). Practically, this generally means eligibility for CGT relief, is available to all TRIS regardless of balance and all individuals with retirement income streams that have a combined balance over $1.6million.

The segregated method

The segregated assets approach for exempt current pension income (ECPI) under section 295-385 of the Income Tax Assessment Act 1997 (ITAA97) is one of two methods that can apply. A segregated asset approach allows ordinary and statutory income derived from assets which satisfy segregated current pension liabilities to be exempt from tax.

When has an individual segregated their assets?

Practically an individual has segregated their assets when trustees have specified assets of the fund to support the member’s retirement income stream and accumulation interests. As per the ITAA97, the assets are invested, held in reserve, or otherwise dealt with at that time to solely enable the fund to discharge all or part of its liabilities. Therefore, if an asset only supports a pension it will be classified as a segregated current pension asset.

This commonly occurs when a fund is entirely in pension phase or accumulation phase and will be the most common application of this method. The other time this occurs is when a fund has specifically identified assets to be allocated for each member’s pension and accumulation account.

Note: Any reference to segregated non-current pension assets in legislation or ATO documentation refers to assets that are segregated and not supporting a pension.

The criteria for segregated CGT relief

Section 294-110 of the Income Tax (Transition Provisions) Act 1997 details the criteria that must be satisfied for segregated CGT relief to apply. Note the fund must be a complying superannuation fund at all times during the pre-commencement period.

1. Is the asset segregated on the 9th of November 2016?

a. You must determine if the asset satisfies the definition of solely supporting a pension interest.

i. Is the fund in 100% pension phase?

ii. Did you identify assets to support a pension interest?

iii. Are assets potentially solely supporting a pension interest by way of segregation for member investment purposes?

2. Did the member hold the asset from the 9 November 2016 to 30 June 2017?

a. If so, the member cannot have physically sold the asset during the pre-commencement period.

3. Did the asset cease being a segregated current pension on or before 30 June 2017?

a. This is the ‘cessation time’ (See its application below).

i. Did the member transfer segregated current pension assets back into accumulation phase?

ii. Did the member receive a contribution into an accumulation account that now means the fund’s assets are not segregated current pension assets?

4. Has the member chosen for relief to apply to the asset on or before the fund is required to lodge its 2016-2017 superannuation annual return?

a. The SMSF’s trustees should minute their decisions relating to CGT relief. When lodging the fund’s annual return they will need to fill out the CGT schedule with the appropriate assessable amount. Creation of a detailed asset register of assets to which CGT relief has been applied to should be created and retained as part of the SMSF’s records during this period.

b. A trustee can choose relief for some or all of the funds eligible assets.

If all these elements have been satisfied, the assets are eligible for segregated CGT relief.

Operation and consequences of applying segregated CGT relief

The consequences of choosing to apply CGT relief to assets of a fund that are segregated current pension assets are as follows:

- The fund is deemed to have sold and repurchased the asset at the cessation time.

o The CGT discount period is reset.

- The asset’s cost base is reset to market value at the cessation time.

- The capital gain or loss on the deemed sale is disregarded as the asset, at the time of the deemed sale, was a segregated current pension asset.

- With respect to calculating the fund’s exempt income for 2016/17, once assets are transferred to the accumulation phase the trustee may:

o Continue to adopt the segregated method asset method, or

o Choose to adopt the proportionate method for the entire year. - Future CGT event on sale of the asset.

o Capital gain or loss is based on the reset cost base.

o Exempt amount is based on the ECPI method used at the time of sale.

Cessation time

For the segregated approach, the timely factor is the triggering of the cessation time. As soon as any value is transferred back into accumulation or a contribution is received so all or some of the fund’s assets cease being segregated current pension assets, this is the point from when taxation outcomes will be determined.

There are scenarios where a contribution received by a fund in full pension phase will trigger a cessation date but it will depend upon the action of the trustees. Where a contribution is made to an SMSF which is 100% in pension phase, it cannot be added to a pension account so therefore it will always create an accumulation interest for the member.

A trustee can ensure this contribution does not force a cessation date by ensuring it is classified as a segregated non-current pension asset on receipt.

Whether the contribution is converted to fund an income stream immediately or maintained in an accumulation account, the trustees will still need to separately identify and treat the amount as a “segregated non-current asset” as defined by s295-395 ITAA97 to ensure that the SMSF assets continue to meet the definition of ‘segregated current pension assets’ in accordance with s295-385 ITAA97 with respect to the members’ pension account(s).

This can be done in the form of a trustee minute and will eliminate any doubt of the trustee’s intention to maintain segregated pension assets. Inaction by the trustees to separately identify the contribution, will result in the fund’s assets being treated as unsegregated as the fund would have no longer ‘solely’ funded pension liabilities when the contribution is received.

Practical applications of the cessation date would include:

- A two member fund which has members in full pension phase at 9 November 2016. Both members have balances over $1.6 million. One member receives a $25,000 contribution on 1 May 2017.

o This will be the cessation time for CGT relief and the consequences above will apply.

o UNLESS on 1 May 2017 the members choose to start to segregate assets between segregated current pension assets and segregated non-current assets (i.e. assets not supporting an income stream) and this is evidenced by a minute.

In this instance, this would mean segregating the contribution received as a non-current asset that is supporting the accumulation interest created. Therefore, the fund’s existing assets have still not ceased to be segregated current pension assets.

o If the members did not choose to segregate assets, all of the fund’s assets would cease being segregated current pension assets as the assets now support both accumulation and pension interests. - The rolling back of funds to accumulation phase to comply with the transfer balance cap on any date in the pre-commencement period.

Note triggering a cessation time before 30 June 2017 does not force members have to roll back their pension account to under $1.6 million on that date. It just means that taxation consequnces and the cost base reset will occur on this date.

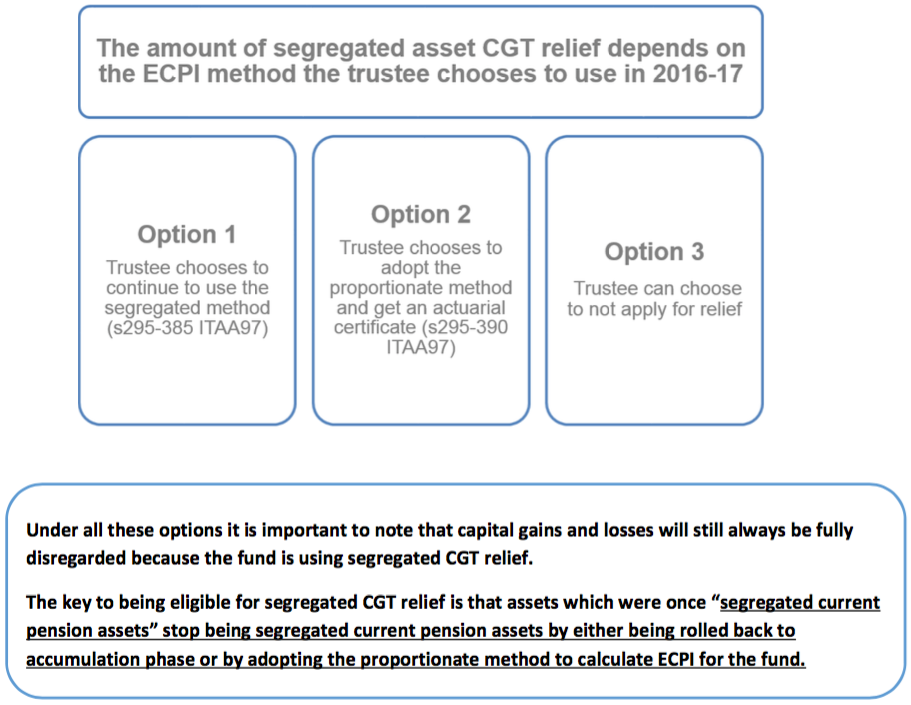

The options under segregated CGT relief

Assets which were segregated current pension assets on 9 November 2016 (the ‘pre-commencement period’) must use the segregated method to claim CGT relief. However, trustees have the below three options for how the CGT relief is structured in 2016/17.

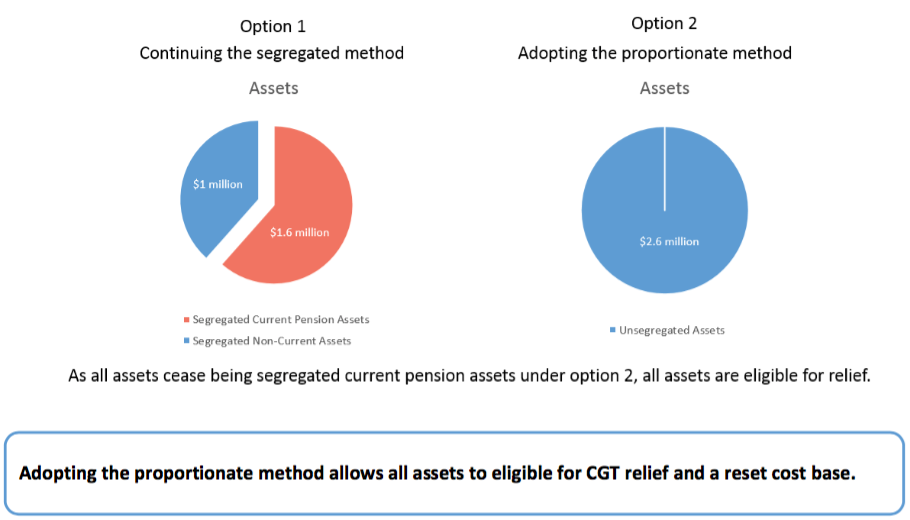

The next image illustrates how option 1 (continuing the segregated method) and option 2 (adopting the proportionate method) work regarding the assets which will be eligible for CGT relief. Under option 2, the trustee chooses to pool together all of the fund’s assets across all pension and accumulation interests to comply with the TBC or TRIS reforms. In essence, all of the fund’s assets are no longer segregated current pension assets and are all eligible for CGT relief under the segregated method.

Under option 1, the trustee selects one or more specific segregated current pension assets to transfer out of pension phase and into accumulation phase in order to comply with the changes. The asset(s) which were transferred to accumulation phase will be the only asset that is no longer a segregated current pension asset and is eligible for CGT relief under the segregated method.

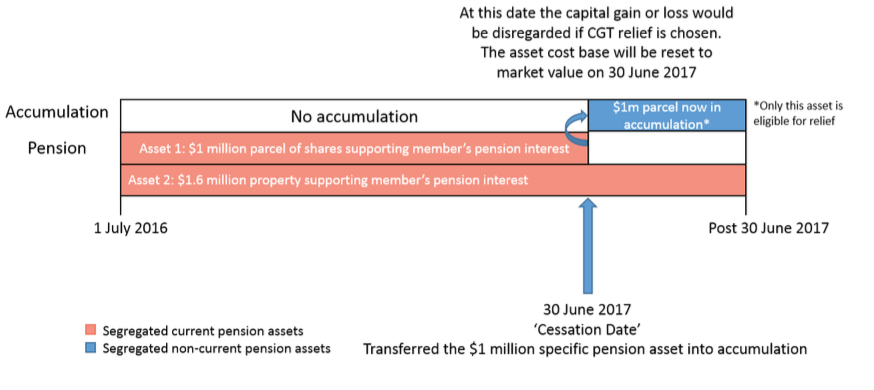

Option 1 – Continue using the segregated method

Under this option, the trustee selects a specific segregated current pension asset to transfer out of pension phase and into accumulation phase in order to comply with the changes. The asset which is transferred to accumulation will be the only asset that is no longer a segregated current pension asset and is eligible for CGT relief under the segregated method. The remaining pension assets continue to be treated as segregated current pension assets and do not benefit from any cost base reset.

The previous image illustrates the scenario where a trustee has specifically transferred an asset into accumulation to comply with the TBC reforms such that it becomes a segregated non-current asset and ceases being a segregated current asset. The trustee has decided not to adopt the proportionate method and therefore all assets are not eligible for relief. They may decide this because they want to keep members’ assets separate.

A fund that is 100% in pension phase via TRISs would also fall into this category. If on 1 July 2017, the TRIS is not in retirement phase then all of the funds’ assets would cease being segregated current pension assets. In this scenario they would become accumulation assets or segregated non-current assets. A TRIS in retirement phase occurs when a member is 65 years of age or they have notified the fund they have met a condition of release with a nil cashing restriction.

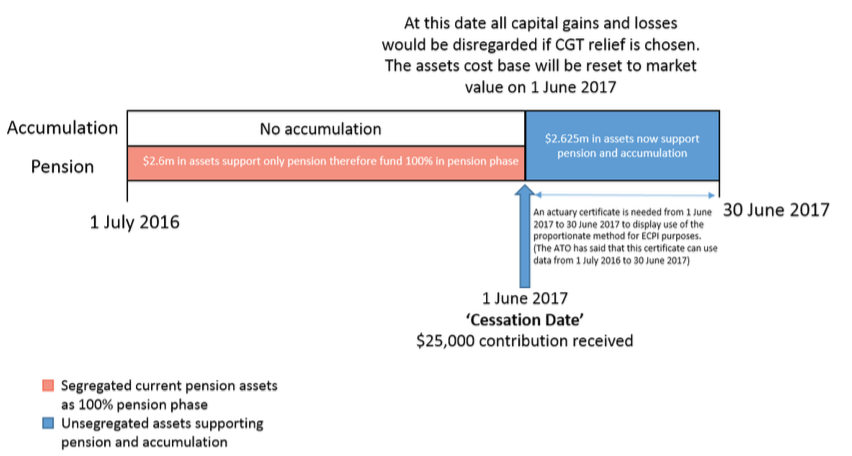

Option 2 – Adopt the proportionate method prior to 1 July 2017 (Recommended just prior to 1 July 2017)

Under this option, the trustee chooses to pool together all of the fund’s assets, across all pension and accumulation interests to comply with the TBC or TRIS reforms. In essence, all the fund’s assets are no longer segregated current pension assets and are all eligible for CGT relief under the segregated method. The fund is not using the CGT relief provisions relevant to the proportionate method, even though the fund will now apply the proportionate method in determining its overall ECPI. The fund may be required to get an actuarial certificate to support its use of the proportionate method in 2016/17 and future income years.

This option is likely to provide the best outcome for funds with segregated assets on 9 November 2016. It allows the trustee to lock in and disregard any unrealised capital gain across all segregated assets at cessation time. The below image illustrates how the adoption of the proportionate method applies. The fund is in 100% pension phase until a contribution is received on 1 June 2017. The trustee chooses not to segregate this contribution into an accumulation sub-account. Therefore all assets now support pension and accumulation accounts and therefore cease being segregated current pension assets. They now become unsegregated assets.

The same results ensue when a transferring of funds back into accumulation triggers a cessation date.

An actuarial certificate is required to determine the fund’s ECPI for the time period after this date. (As all income and gains are disregarded before 1 June 2017), in this example from 1 June 2017 to 30 June 2017.

For pragmatic and efficiency reasons, the ATO is allowing actuaries to use data for the whole financial year to determine the ECPI percentage that is required from 1 June onwards in this example.

The above scenario can also apply to trustees that specifically segregate pension assets if they decide they no longer want to segregate. A trustee may choose to adopt the proportionate method and roll back the value needed to comply with the TBC rather than a specific asset. This will force all assets to be eligible for CGT relief because the trustee will now have unsegregated assets going forward.

Option 3 – Choose for CGT relief not to apply

The fund could also choose not to apply the CGT relief to some or all of the assets that would otherwise qualify. Under this option no deemed sale and reacquisition of the asset occurs and the asset’s original cost base is maintained going forward. Any capital loss or gain realised on a future CGT event happening with respect to the asset will also be determined using the original cost base.

This will be a relevant choice for assets which currently have a large capital loss. There would be no benefit in resetting the cost base as the carry forward capital loss would be disregarded and its offsetting benefit lost.

Note: These consequences would equally apply to a fund where a trustee makes an invalid choice to apply for CGT relief. For example, where a trustee does not make a choice in the approved form before the date the fund’s 2016/17 income tax return is due.

Choosing the method of calculation of CGT relief and annual ECPI

As seen above there is no obligation between the way in which an SMSF trustee is eligible to access the transitional CGT relief based on its make up on 9 November 2016 and the method adopted to calculate the exempt current pension income (ECPI) of the fund for the 2016/17 financial year. In other words, if the SMSF is effectively using the segregated approach at 9 November 2016 because all of the SMSF assets are supporting income streams, the SMSF trustees are not precluded from electing to use the proportionate method at some later time in order to calculate the ECPI of the fund for the 2016/17 financial year. In fact, for some funds, this combination of choices has a very beneficial application of the transitional relief. This is clearly outlined in both the Explanatory Memorandum accompanying the introductory legislation and the Australian Tax Office’s Law Companion Guideline 2016/8 as an acceptable application of the rules, as described in Option 2 above.

Summary of choices

There are some significant decisions that need to be made by trustees in electing for CGT relief to apply.

Future ECPI

The future retirement phase make up of your fund does not need to be a consideration with the segregated CGT method. As all gains are disregarded you cannot get a better result in the future than what will currently be on offer.

Capital Losses

It should be noted when an asset has sustained a capital loss there appears to be no advantage in making an election to reset the cost base of the asset. Capital losses under the segregated method are completely disregarded. Care must be taken that CGT relief is not blindly applied to all assets under this method.

Unit trust structures

For SMSFs with units in private trusts or companies the cost base reset will also apply. However, the cost base reset will only apply to the unit/shares and not the underlying assets held by the unit trust or company. Therefore a higher taxable amount may flow through to the SMSF than desired on sale of the assets in the trust or company. Consideration then should be given to timely winding up of the trust.

Prohibition of the use of the segregated method and member investment choice

Although the option to continue to use the segregated method is available to trustees in 2016/17, segregation for tax purposes may not be available for future income years. From 1 July 2017, SMSFs under the following conditions will be prohibited from using the segregated method for tax purposes:

- the fund is an SMSF or Small APRA Fund (SAF) at any time during the income year;

- at any time during the year there is at least one interest in the fund in the retirement phase; and

- all of the following apply:

o just before the start of the income year a member of the fund has a total superannuation balance that exceeds $1.6m; and

o that member is a recipient of a superannuation retirement phase income stream (whether in an SMSF, SAF or another superannuation provider);and

o at any time of the year that member has a superannuation interest in the fund.

Therefore, from 1 July 2017, SMSFs which fit the above criteria will have to use the unsegregated method for purposes for calculating ECPI going forward.

It is important to understand that those funds which are prohibited from using the segregated method to calculate ECPI for the 2017/18 and later financial years are not limited when making choices concerning how the SMSF’s assets are held and how asset allocation decisions are made.

The proposed limitation on the use of the segregated method as a means of calculating ECPI has been introduced as part of an anti-tax avoidance measure limiting the transfer of assets between accumulation and retirement phase in order to manipulate the tax outcomes on disposal of assets.

The measures do not limit members of an SMSF making individual investment choices. Equally, SMSF trustees are free for investment purposes to maintain different pools of assets as a consequence of those investment choices made by members. In other words, “segregation” for investment and asset allocation purposes is acceptable in the 2017/18 and later financial years.

SMSFs subject to the new rules may decide it is more commercial to start using the proportionate method sooner. For example, on 30 June 2017 or earlier, as a consequence of the creation of a new accumulation interest in compliance with the $1.6 million transfer balance cap. Anecdotal evidence suggests many SMSFs currently find it more cost efficient to use the proportionate method.

Anti-avoidance

The ATO will also be applying Part IVA for schemes which do more than is necessary to comply with the TBC or TRIS changes. Therefore any schemes which are designed to abuse CGT relief will be scrutinised.

The arrangements that the Commissioner will scrutinise carefully will exhibit the following features:

- they place the taxpayer in a position to make the choice,

- they go further than is necessary to provide temporary relief from CGT for members complying with the reforms commencing, and

- they exhibit contrivance of manner, a lack of correspondence of form with substance, or other matters relevant under section 177D of the ITAA 1936, that point to the purpose of avoiding tax.

We note some examples that potentially could be scrutinised by the ATO:

o Setting up a TRIS post 9 November 2016 and ceasing it after 30 June2 017 purely to gain the uplift in cost base values. However, setting up a genuine pension after 9 November 2016 will not necessarily be considered tax avoidance and SMSF trustees can utilise the CGT relief if the TRIS continues.

o Transferring assets out of the segregated current pension class in excess of what is necessary to comply and also transferring other fund assets into the segregated current pension asset class to maintain a pension near the level of $1.6 million.

All of these arrangements are conducted purely for a tax benefit and provide no change in the economic position of the taxpayer and therefore should be conducted with great care. You should always ensure that whatever strategies you recommend to your clients in implementing the transitional CGT relief are acceptable to your clients and that they fully understand any risks that may be inherent in adopting those strategies, if any.

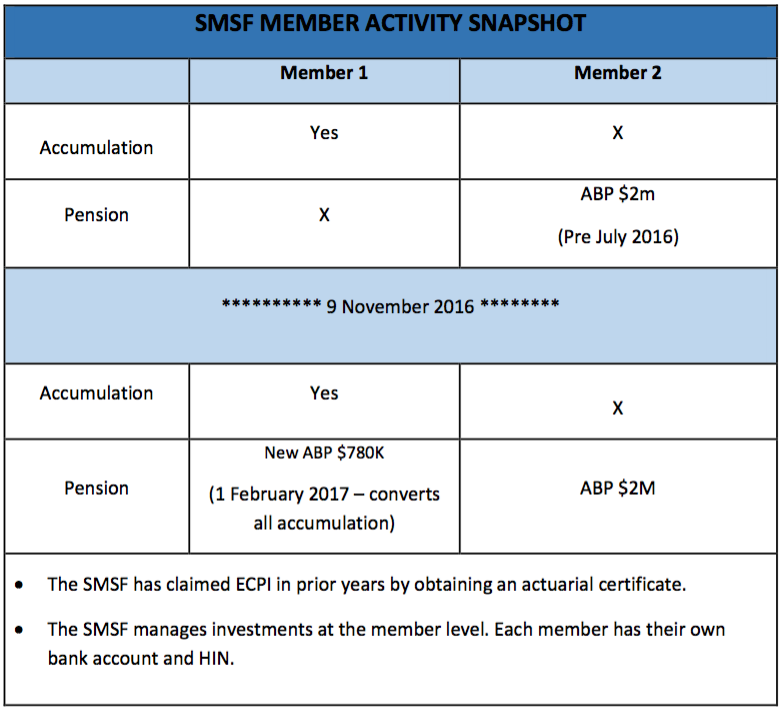

A fund which segregates for investment purposes on a member level

Consider a fund where each member manages their own investments (Ie. for investment purposes). Each member has their own bank account and their own HIN number for their shares. In previous years, the SMSF has claimed ECPI on the unsegregated method via an actuarial certificate as the fund has never been in full pension phase and members don’t specifically segregate assets to support accumulation and pension.

Member 1 only has an accumulation account on 9 November 2016. Member 1 starts a pension with all his assets on 1 February 2017.

Member 2 only has a pension account on 9 November 2016.

Despite being able to use the unsegregated method to calculate ECPI, as the fund has a mixture of accumulation and pension accounts, this may not be the case for CGT relief.

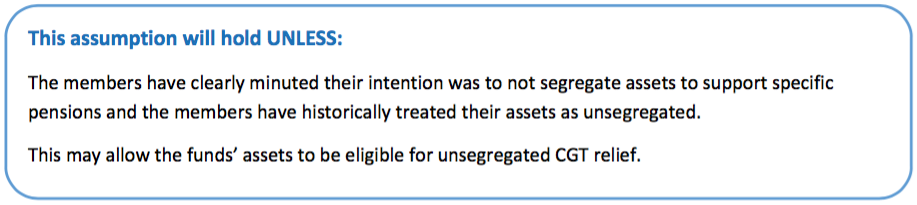

There will be a predetermined assumption that as Member 1 and Member 2 track their assets separately to each other, whilst any member only has a pension account it is arguable that the member has set aside 100% of their assets to solely support its pension liabilities. These assets could satisfy the definition of segregated current pension assets. This in turn will limit the fund’s ability to access CGT relief under the unsegregated method (s294-115).

Therefore under this assumption:

Member 1 – Will not be eligible for segregated CGT relief as they did not have any segregated current pension assets on 9 November 2016. They will not be eligible for unsegregated CGT relief because at some stage during the pre-commencement period (1 February 2017) the member had segregated current pension assets. (See the SMSF Association Go-To Guide for more information on unsegregated CGT relief)

Member 2- Will be eligible for segregated CGT relief as they satisfy the relevant criteria, most notably having assets that satisfy the definition of segregated current pension assets.

Disclaimer

This document contains general advice only and is prepared without taking into account particular objectives, financial circumstances and needs. The information provided in this article is not a substitute for legal, tax and financial product advice. Before making any decision based on this information, you should assess its relevance to the individual circumstances of your client. While the SMSF Association believes that the information provided in this article is accurate, no warranty is given as to its accuracy and persons who rely on this information do so at their own risk. The information provided in this bulletin is not considered financial product advice for the purposes of the Corporations Act 2001.