This Superannuation Reference Guide brought to you by the SMSF Association provides a clear & concise overview of all the super contribution changes that you need to be aware of. The Superannuation Reference Guide covers the following topics:

- Super Contributions

- Super Benefit Payments

- Super Income Stream Benefits

- and the $1.6m transfer balance cap

Download the SMSF Association Superannuation Reference Guide: ![]()

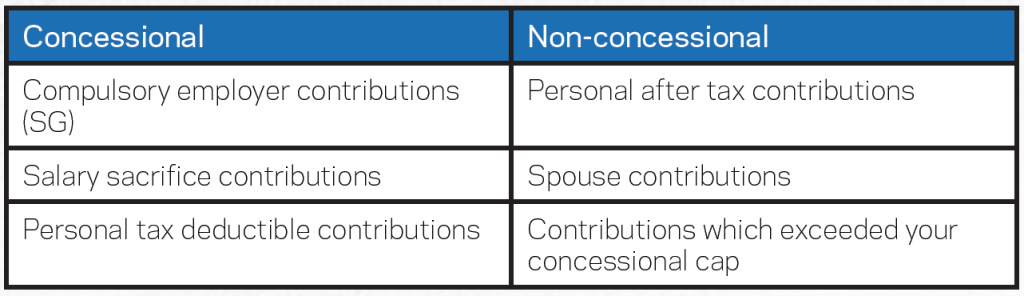

Superannuation Contributions

- Contributions are counted towards the caps in the year in which the cash is received into the fund’s bank account.

- A tax deduction can be claimed for personal contributions if income from employment related activities is less than 10% of total income.

- In 2017/18, the 10% rule is removed for personal tax deductible contributions.

- To claim a tax deduction for a super contribution, you must notify your super fund in writing in the approved form as required by s290-170 of the ITAA 1997.

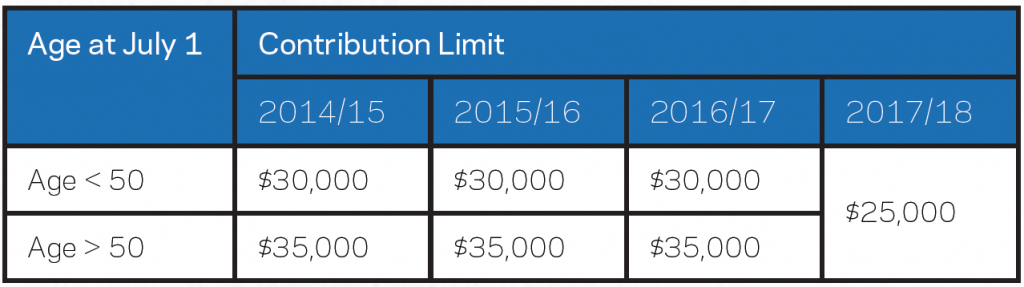

Concessional Contributions (CC)

Information on the 2016/17 changes to Concessional Contributions can be found in our blog post, Year End Superannuation Planning – 2016/17 Financial Year

Non-Concessional Contributions (NCC)

- Aged under 65 at 1 July may ‘bring forward’ two years of contributions (i.e. 3 x annual cap).

- Aged over 65 at 1 July is restricted to the annual limit.

- Post 1 July 2017, taxpayers with a total super balance over $1.6 million will not be able to make NCCs.

- If the bring forward provision is triggered in or before 2016-17 but the full $540,000 amount is not used, then the bring forward cap available in 2017-18 and 2018-19 will be reduced.

- Taxpayers who are approaching a balance of $1.6 million will have their ability to use the bring forward rule reduced.

Non-Concessional Contributions Cap Exemptions

- Proceeds from settlement of personal injury.

- Government co-contribution payments.

- Rollovers from taxed superannuation funds.

- Proceeds from sale of small business asset.

Excess Contributions Tax

- ECC will count towards your NCCs cap. This can be avoided by electing to release the ECC.

- May elect to withdraw 85% of the ECC to pay the tax debt.

- Complete the ENCC election form to withdraw ENCC and earnings from the fund.

- Associated earnings is calculated on the current general interest charge rate.

Contributions Tax For Higher Income Earners

Division 293 tax of 15% will be charged to CCs above the $300,000 threshold.

- For the 2017/18 year onwards the threshold amount will be $250,000.

- Adjusted Taxable Income (ATI) > $300,000 then additional tax of 15%.

- ATI = ISP – RSC + LTC

– ISP includes: taxable income, reportable fringe benefits, investment loss & RSC

– RSC includes: reportable superannuation contributions (eg: salary sacrifice)

– LTC includes: CCs less excess contributions

- CCs that exceed the CC cap won’t be subject to Div 293 tax.

Spousal Contributions

- Members can claim the maximum tax offset of $540 when their spouse’s income is $10,800 or less (Phases out at $13,800). The spousal income threshold will increase to $37,000 from 1 July 2017.

- Spousal income includes assessable income, total reportable fringe benefits and reportable employer super contributions.

Government Co-Contributions For 2016/17

Contribution Eligibility

- Work test before making contributions is to work 40 hours in a 30 day period.

Superannuation Benefit Payments

Preservation Of Benefits

- An individual must reach their preservation age before they can access their superannuation benefits.

Conditions Of Release

Superannuation monies can only be withdrawn when a member meets a condition of release. The following are legislated conditions of release:

Superannuation Income Stream Benefits

Minimum & Maximum Annual Payments

Taxation Of Income Streams

- Tax free component is not taxed. Taxable component is taxed as follows:

- On 1 July 2017, an individual on a TTR who has not met a condition of release won’t satisfy as an income stream in retirement phase and won’t garner ECPI.

Superannuation Lump Sum Benefit Payments

- Low rate cap amount is $195,000 in 2016/17

Superannuation Death Benefit Payments

Lump Sum Death Benefit Payments

- Lump Sum Death Benefits paid to tax dependants are tax free in the hands of the tax dependant.

- Tax free component of the lump sum is not taxed. Taxable component of the lump sum is taxed as follows:

Income Stream Death Benefit Payment

- Income streams death benefits cannot be paid to non-dependants.

- Tax free component is not taxed. Taxable component is taxed as follows:

$1.6 Million Transfer Balance Cap

- All members who are receiving a pension on 1 July 2017 will have a transfer balance cap of $1.6 million created at that time.

- The cap operates on the basis of “credits” counting to the cap and “debits” removing value from the cap.

Excess Transfer Balance Tax

- Going over the $1.6 million transfer balance cap will require the excess amounts to be commuted.

- Excess amounts will also attract “notional earnings” which count towards the transfer balance cap. Notional earnings are charged at the 90 day bank accepted bill rate plus 7%.

- An excess transfer balance tax of 15% applies to the notional earnings.

Capped Defined Benefit Income Streams

- A life-time pension or annuity’s special value is the individuals annual entitlement multiplied by 16.

- A non-commutable life expectancy or market-linked product. The individuals special value is their annual entitlement multiplied by the product’s remaining term (rounded up).

- An individual’s ‘defined benefit income cap’ is their general transfer balance cap for the financial year divided by 16.

- Exceeding the DBIC will result in additional income tax.

If you would like to know how the $1.6 million transfer balance cap may affect you, see our SMSF Checklist on the $1.6 million Transfer Cap.

A downloadable version of the Super Reference Guide can be found here: